In a new display of fiscal discipline and market confidence, President Javier Milei'sgovernment achieved a resounding success this Wednesday in the peso-denominated debt auction, managing to absorb 700 billion pesos and refinance its commitments at 114.66%. The operation represented a key relief ahead of the Buenos Aires elections, where economic stability is one of the essential pillars of the official strategy.

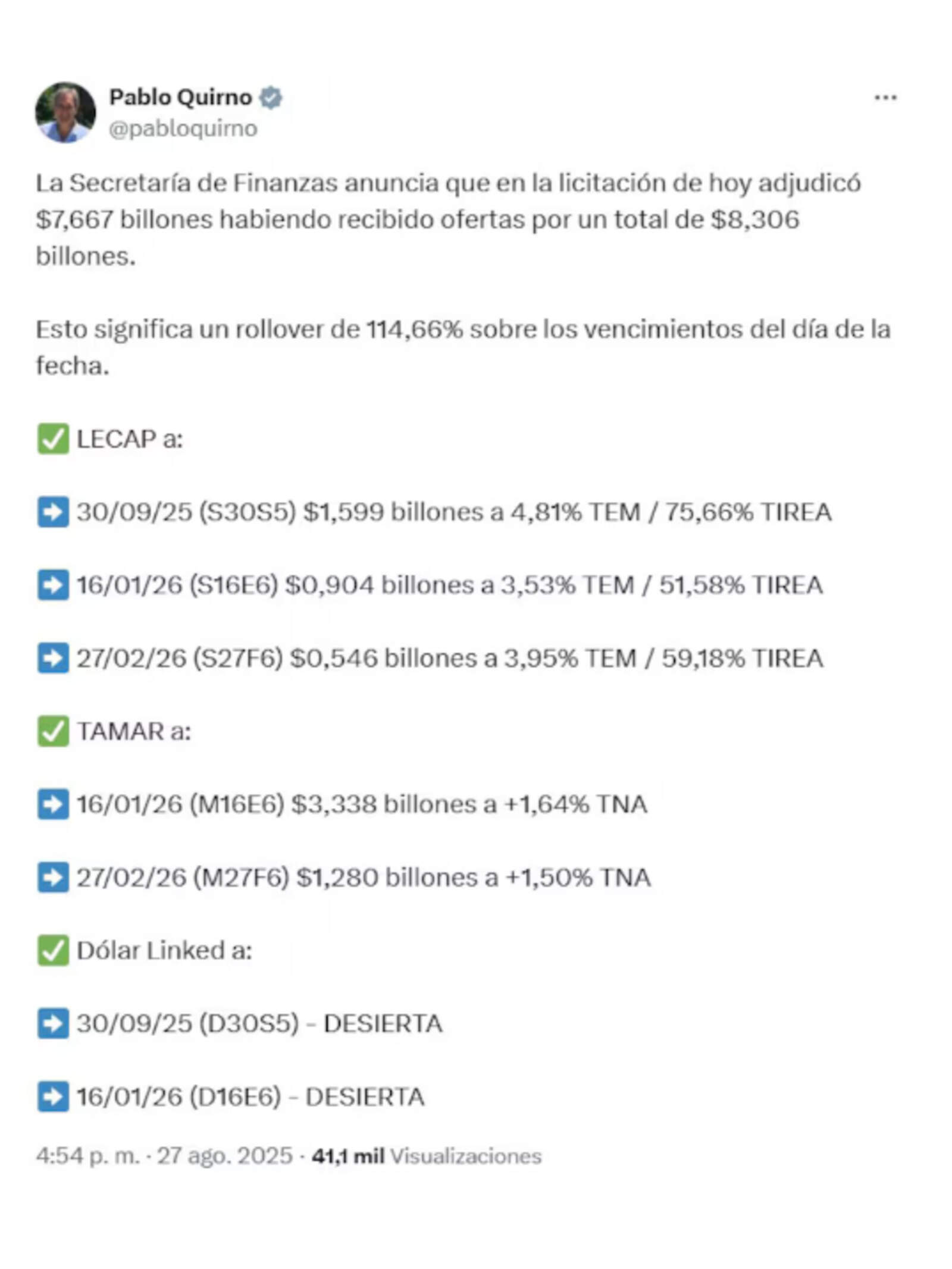

The Ministry of Economy reported that the auction concluded with awards totaling 7.67 trillion pesos, out of a total of 8.3 trillion pesos in bids, a figure that comfortably exceeded the maturities reduced to 7.7 trillion pesos thanks to previous cleanup measures. Finance Secretary Pablo Quirno celebrated that the Treasury not only refinanced all its commitments but also secured additional financing in a context of competitive rates.

Luis "Toto" Caputo

The auction stood out for the marked market interest in medium-term instruments, reflecting confidence in the administration's economic policy. In particular, 1.59 trillion pesos in Lecap maturing in September 2025 were placed, 0.9 trillion pesos in Lecap maturing in January 2026, and 0.54 trillion pesos in Lecap maturing in February 2026. Meanwhile, bonds adjusted by TAMAR concentrated the highest demand: 3.34 trillion pesos maturing in January 2026 and 1.28 trillion pesos maturing in February 2026. In contrast, dollar-linked options were left deserted, an indication of controlled expectations regarding the exchange rate.

The government's strategy was clear: to prevent immediate maturities from generating pressure on the money market and to ensure an orderly process ahead of the elections. To this end, the Central Bank supported the operation with technical measures, including changes in the composition of reserve requirements and a staggered increase that will take effect on September 1. These changes will allow banks to integrate higher percentages with public securities, ensuring liquidity and supporting demand.

Quirno en X:

Private consulting firms agreed that the official maneuver proved effective. Portfolio Personal Inversiones (PPI) highlighted the unusual trading volumes in BONCAP maturing in February, which soared to 474 billion pesos, almost tripling the previous high. The report suggested that this dynamic was due to a preventive intervention by the Central Bank to contain yields and ensure a favorable framework for the auction.

Meanwhile, Cohen emphasized that the auction was intelligently designed: a single short-term alternative with Lecap S30S5 and a menu oriented toward longer terms, in line with the need to extend duration and clear commitments. "Everything suggests that the government's strategy would aim to extend maturities and provide greater predictability," the consulting firm stated.

In the secondary market, the response was also positive: CER bonds led with increases of 1.3%, while the fixed-rate curve advanced 0.9%, with a notable yield compression of 3.7 percentage points to an average of 51% nominal annual rate.