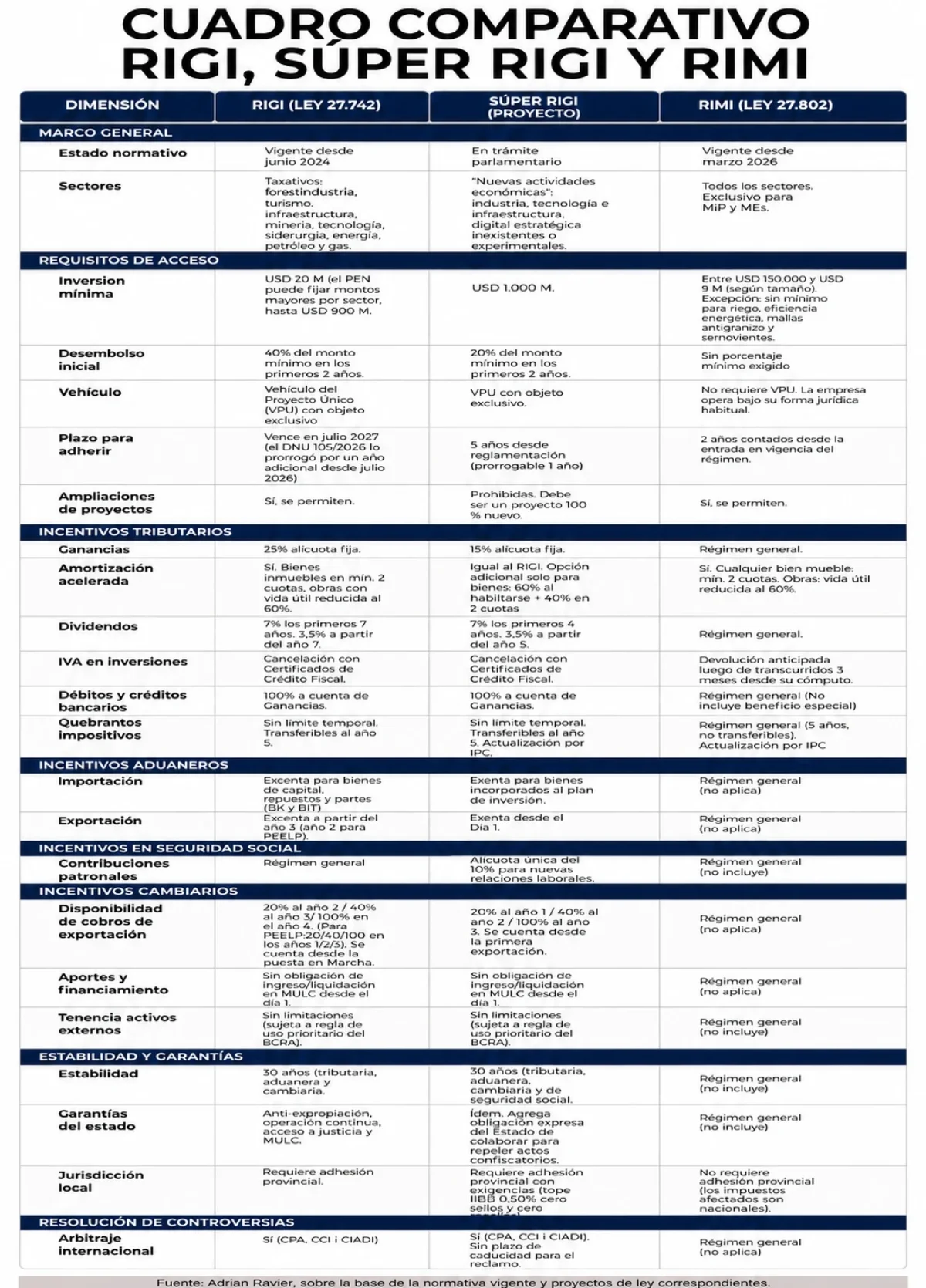

In less than two years, Javier Milei's administration has launched three regimes aimed at promoting investments that encompass practically the entire business framework: from a small and medium-sized enterprise (SME) interested in modernizing its equipment to a global technology company analyzing the installation of a semiconductor center in the country. Each instrument responds to a specific scale, logic, and set of advantages.

Through the RIGI, RIMI, and the Super RIGI initiative, Argentina seeks to organize a gradual scheme of incentives according to the investor's size: large projects starting from USD 200 million, medium investments from SMEs starting at USD 150,000, and new industries with a minimum of USD 1 billion. The framework includes tax benefits, adherence conditions, and, for the RIGI, regulatory predictability for 30 years.

The adoption of these regimes occurred after decades of interventionism that consolidated an adverse scenario for private capital: export rights, currency controls that hindered the remittance of profits or obtaining foreign currency, a high tax burden, and regulatory instability that made the modification of rules during the game a common occurrence.

After decades of interventionism, Argentina had to reverse an unfavorable context for private investment

While other nations attracted large-scale projects in energy, mining, technology, and infrastructure, Argentina maintained a framework that discouraged long-term capital placement due to regulatory volatility, state intervention, and a loss of confidence in contract enforcement.

Against this backdrop, starting in 2024, the system of incentives promoted by the national government began to take shape.

These three instruments do not overlap; rather, they function complementarily. Each one addresses a different segment of the investor universe and, together, they form a tiered structure by amount and activity: from the small business updating its equipment to the international capital studying the establishment of an industry that does not yet exist in the country.

RIGI: Large-scale investments in strategic areas

The first piece was the Regime of Incentives for Large Investments (RIGI), established by Law 27,742 —the Framework Law—, approved in July 2024 and regulated by Decree 749/2024. The regime was aimed at initiatives with a minimum outlay of USD 200 million in eight sectors: forestry, tourism, infrastructure, mining, technology, steel, energy, and oil and gas. It includes tax, customs, and exchange benefits, along with regulatory stability for 30 years.

Entry into the regime requires at least USD 200 million per project and the execution of a minimum of 40% within the first two years

To enter, a minimum investment of USD 200 million per project is required, and at least 40% must be executed within the first two years. Additionally, each initiative must be organized through an independent company, established solely for that purpose and separate from the investor's other businesses: the Unique Project Vehicle (VPU).

VPUs must allocate at least 20% of the total investment to payments to local suppliers. The period for applying for adherence was set to end in July 2026 but has been extended by one year. The interested party must submit a plan to the Implementing Authority, which has 90 business days to evaluate it and decide on its approval or rejection.

A broad range of benefits

On the tax front, VPUs are subject to a fixed rate of 25% for Income Tax, 10 points lower than the general system. They can also apply for accelerated depreciation: movable assets are accounted for in no less than two annual installments, while infrastructure works use a reduced useful life of 60%.

The scheme also allows for the deduction of losses without expiration, in contrast to the common regime, which only allows them to be carried forward for five years. For projects with extensive construction and commissioning phases, this limitation is particularly detrimental, as losses can accumulate beyond that period.

The RIGI allows the use of VAT Tax Credit Certificates to avoid keeping capital immobilized while the project is being constructed

In the first five years from adherence, VPUs will be able to deduct interest without limit, as the RIGI has eliminated the restrictions applicable in the general regime. Regarding dividends, the rate is 7% during the first seven years and reduces to 3.5% from the seventh year.

Regarding VAT, the RIGI accepts Tax Credit Certificates that prevent funds from being withheld during the construction phase. Additionally, 100% of the Bank Debits and Credits Tax paid can be counted as a credit against Income Tax.

In customs, imported goods incorporated as assets of the venture are exempt from import duties. Sales abroad are exempt from withholdings starting from the third year after adherence; for Long-Term Strategic Export Projects (Peelp), the benefit begins in the second year.

The express adherence of each province is necessary for projects located in its territory to receive these advantages

On the exchange front, income from exports gradually acquires free availability: 20% in the second year, 40% in the third, and 100% in the fourth, calculated from the start of the VPU. For Peelp —initiatives of at least USD 1 billion per stage and with a minimum of 70% of their production destined for export— the schedule is accelerated: 20% in the first year, 40% in the second, and 100% in the third, in addition to the elimination of withholdings starting from the second year.

From the outset, capital contributions and financing are not required to enter or settle in the exchange market. Therefore, the investor can keep those resources in the currency and jurisdiction of their choice.