Mortgage credit reached 44,305 loans in 2025, represented 20% of operations in CABA and 15.9% in the Province of Buenos Aires, mobilized USD 3,679 million and registered annual rates of 5.2% with average terms of up to 25.8 years.

Agregar La Derecha Diario en

Compartir:

Mortgage credit inArgentina experienced strong growth in 2025, positioning it as one of the best years since records existed, reflecting a structural change after a prolonged period of stagnation. With a total of 44,305 loans granted, the year closed as the fourth best since 2004, only behind the historic peaks of 2017, 2018 and 2007, marking a turning point in access to housing and in the dynamics of the real estate market. According to a report by the Urban Fabric organization, the recovery was not only expressed in the volume of operations, but also in the recentralization of mortgage credit within the financial system, consolidating in 2025 a phase of operational normalization after years of

virtual inactivity.

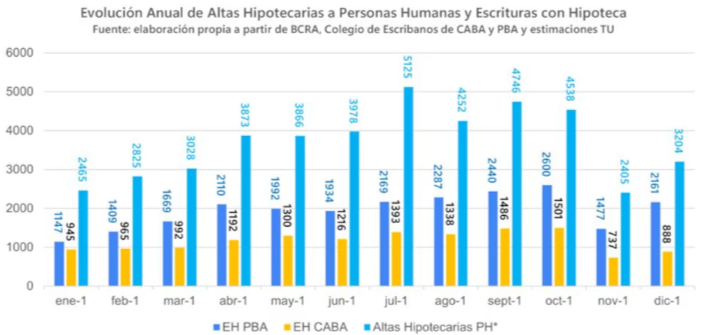

In the Province of Buenos Aires, the phenomenon was significant: 147,393 deeds were registered, of which 23,395 transactions (15.9%) were carried out through mortgage credit. The total volume mobilized reached USD 2,390 million, with an average ticket of USD 102,000. “From a time point of view, 2025 was marked by some volatility towards the last part of the year. November showed a slowdown associated with electoral uncertainty, but December closed with a clear uptick, returning to levels similar to those of July. The annual peak was reached in October, with 2,600 mortgage deeds, while December ended with 2,161 transactions, consolidating a solid closing,”

said Tejido Urbano. Annual increase in mortgage registrations and mortgage deeds In the Autonomous City of Buenos Aires, growth was even more pronounced: from less than 5,000 mortgage deeds in 2024 to 13,953 in 2025.

Thus, credits accounted for

20% of transactions, mobilizing USD 1,420 million with an average of USD 101,000 per transaction.

The behavior of the average ticket in the capital showed a particular dynamic. After several months of decline between June and November, December registered a sharp jump, from USD 89,000 to USD 113,000 in just one month, evidencing a recovery in demand at the end of the year.

October once again stood out as the busiest month, with 1,501 mortgage deeds, driven by early decisions in an electoral context. In general terms, the end of the year was at levels similar to those at the beginning of 2025, consolidating a new level of activity with greater prudence

in the market.

“Mortgage credit is back. The challenge ahead is no less: maintaining volume, expanding access and resolving the bottlenecks that today continue to limit the flow of funding to large sectors of the middle class. The discussion is no longer whether credit exists, but how far it can scale and who it can include in the next stage,” the report analyzes

. The average interest rate started 2025 at 5.2% per year, rose through September and then fell.

Rates, terms and financing: a system that is being reordered Credit conditions also reflected

the new scenario. The average interest rate started 2025 at 5.2% per year, increased until September and then fell, driven by Banco Nación's active policy with more accessible lines

.

The average term was extended from 23.6 to 25.8 years, a key strategy to facilitate access to credit in a context of greater demand on approval criteria.

“This extension is no small: it responds to strategies and the need to comply with the quota-income relationships required for the approval of loans. In fact, the deadline became one of the main adjustment variables to expand the universe of eligible households already limited by the tightening of the bank score to the application portfolios that were being submitted,” said

Tejido Urbano.

Total funding reached USD 3,679 million, with variable-rate schemes (more than USD 3.2 billion) predominating over fixed-rate schemes (USD 434 million). The monthly flow ranged from USD 233 million at the beginning of the year to USD 275 million in December, consolidating a high level of activity

.

2026: from reactivation to the challenge of scaling

The beginning of 2026 finds mortgage credit in a new phase: without the initial impetus of the rebound, but clearly above the paralysis scenario of previous years. The system seems to have found a stable operating floor, comparable to that of March 2025, which indicates greater regularity in its operation

.

According to the report, the evolution of the year will depend less on demand - which remains firm - and more on the capacity of the financial system to modernize processes, obtain funding and scale up its operations.

In this context, the role of natural persons becomes central. The challenge is to expand the access universe, which involves factors such as the flexibility of scoring, the countercyclical role of Banco Nación, the development of the capital market and new regulations that reduce friction

without losing transparency.

A key turning point came with the digitalization of the system by Banco Nación, which at the beginning of January implemented a completely digital scheme for evaluating and approving mortgage loans.

This change makes it possible to shorten time, reduce administrative costs and eliminate bureaucratic obstacles, in addition to introducing a centralized model that improves scale without losing control of risk. The platform also integrates supply and demand through pre-verified properties and a specific channel for real estate agencies

.

The weight of the public bank is decisive: with more than 20,000 loans granted, it established itself as the main actor in the system in 2025, explaining a substantial part of the growth.

In addition, the expansion of access was reinforced with new lines for mono-taxpayers, incorporating criteria that prioritize the fiscal trajectory over the formal relationship of dependency. The possibility of adding family co-owners and co-signers, together with terms of up to 30 years and differentiated rates, points directly

to historically excluded sectors.

“Together, these signs shape a scenario in which mortgage lending no longer depends exclusively on the immediate macroeconomic situation, but on concrete institutional decisions. The stabilization of variables such as inflation and the exchange rate contributes to improving predictability, but the real margin for growth for 2026 will be given by the capacity to modernize processes, make access criteria more flexible, deepen funding via capital markets and sustain the leadership of public banking,” said Urban Fabric

.

“The system moved again. The question that opens up 2026 is not whether mortgage credit exists, but whether it can be transformed into a financial policy of scale, capable of including more individuals and of being sustained over time without repeating the limits of previous cycles,”