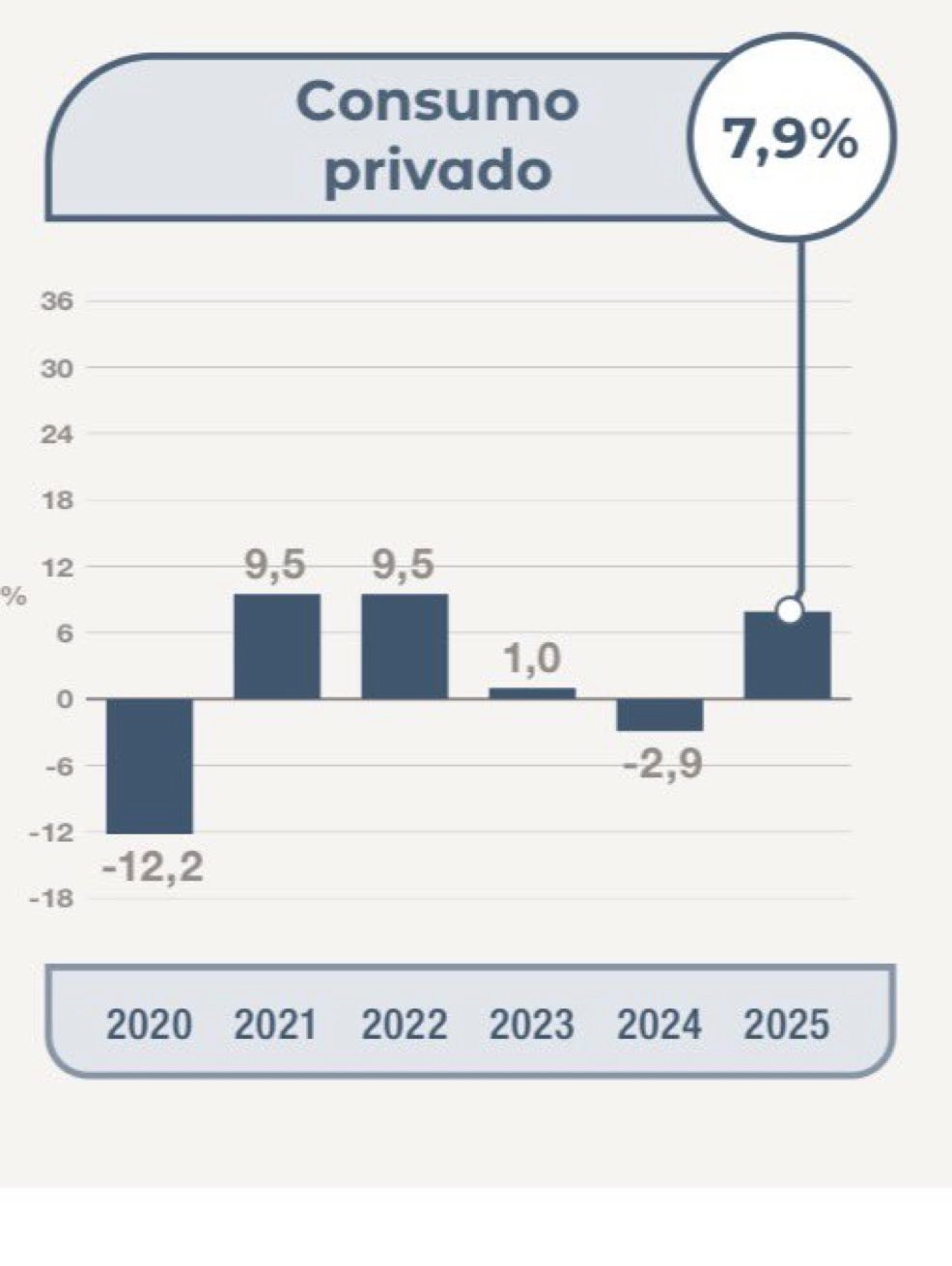

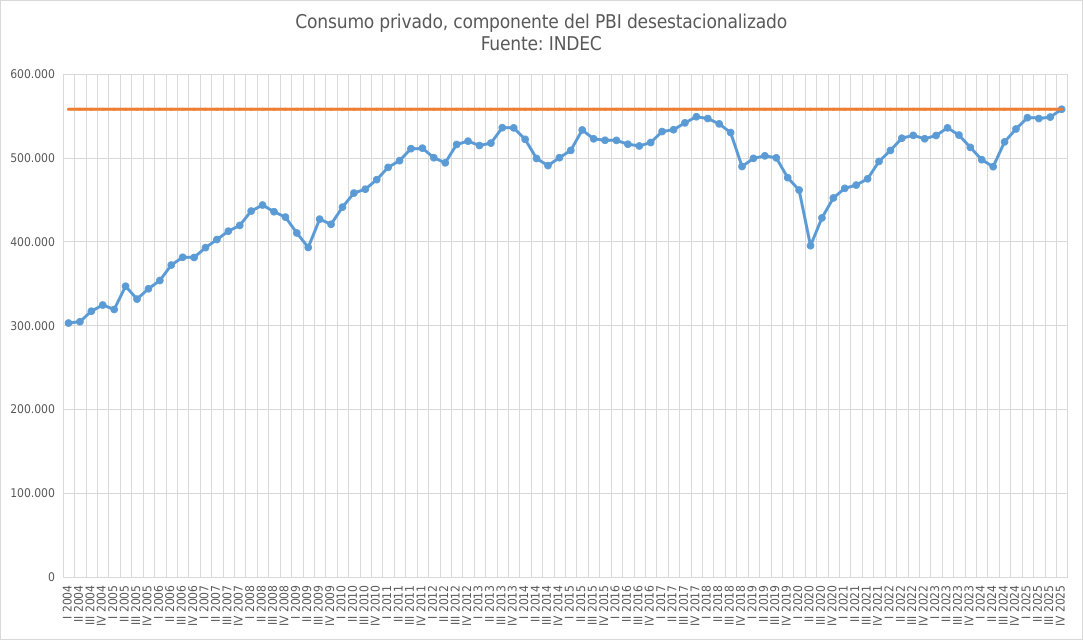

Indec data show that private consumption reached its peak in the series and explained much of the GDP growth of 4.4% in 2025, consolidating itself as the main driver of economic activity.

Nuevo

Agregar La Derecha Diario en

Compartir:

In a context of public debate about the economic situation, official data show a reality different from the perception installed by some analysts and political sectors. According to national accounts, seasonally adjusted private consumption reached its peak in the entire series and in 2025 it grew7.9%, consolidating itself as the main engine of economic recovery. Even on a daily basis, this tendency is beginning to be seen in the activity of cities. Over the past few days, the dynamics observed on the street are consistent with what is reflected in the aggregated data of the national economy

.

According to the National Institute of Statistics and Censuses (Indec), the Argentine economy grew 4.4% in 2025, a result that acquires special relevance for the national government, which projects a sustained recovery towards 2026 after two initial years marked by fiscal adjustment and the attempt to reduce inflation. The year-on-year increase in Gross Domestic Product (GDP) in 2025 was explained by the increase in private consumption (7.9%), public consumption (0.2%), exports (7.6%) and gross fixed capital formation (16.4%). Measured at current prices, private consumption was also the most important component of aggregate demand, accounting for 70.0% of GDP. Behind it were gross fixed capital formation (16.0% of GDP), exports (15.6% of GDP) and public consumption (14.9%

of GDP). Private Consumption

The sectors that drove activity On the

supply side, several key sectors showed significant growth during the year.

Among those with the highest increases, the following stood out:

Financial intermediation: 24.7% year-on-year Mining and quarrying:8.0% year-on-year

Hotels and restaurants:7.4% year-on-year

Agriculture, livestock, hunting and forestry:6.2%

Construction: 4.3% On the contrary, some items showed declines

.

Among them:

Fishing:-15.2% year-on-year

Private households with domestic service:-1.1%

Social and health services:-0.2%

Public administration and defense, compulsory social security plans: -1% The Minister of

Economy, Luis Caputo, celebrated the result on the social network X and highlighted the scope of economic recovery. “GDP at constant prices reached an all-time high in 2025, standing 1.1% above the 2022 average (previous high). 12 of the 16 sectors of activity registered increases compared to 2024. Among them were Hotels and Restaurants (+7.4%), Agriculture, Livestock, Hunting and Forestry (+6.2%) and Construction (+4.3%)

,” he said.

The performance of the last tranche of the year

During the fourth quarter of 2025, GDP registered growth of 0.6% in seasonally adjusted terms compared to the previous quarter.

In that period, the impetus came mainly from:

Exports: increase of 5.0%

Private consumption: increase of 1.7%

In contrast, other components showed declines: Public consumption:

-1.0% Gross fixed capital formation:-2.8%

In the year-on-year comparison, the economy showed an increase of2.1%

during the fourth quarter.

Within the components of demand, exports led growth with an increase of 10.9% compared to the same period of the previous year

.

Among the sectors of activity, the following stood out:

Financial intermediation:17.2% year-on-year

Agriculture, livestock, hunting and forestry: 16.1% year-on-year Fishing:

10.6% year-on-year

Private Consumption Official figures also mark

a break compared to previous years. According to Indec, Argentine GDP had fallen 1.3% in 2024 and 1.9% in2023, so the growth of 4.4% in 2025 represents a reversal of the recent recessive cycle. The agency noted that the dynamism of the year responded largely to the performance of exports and the rebound in private consumption, accompanied by greater demand for imported goods and services, suggesting an increase in general economic activity. However, the report also indicates that some challenges persist, especially in terms of private investment and public spending, which showed weakness at certain times of the year.

Looking ahead to the beginning of the year, some private indicators anticipate a transition scenario after the recovery observed in December.

For January, the consultancy firm Equilibra estimated a stable level (0% year-on-year) in the EMAE, with a monthly drop of 0.8% without seasonality, after the “strong recovery” of aggregate activity in December (+1.8% monthly).

According to analysts at the consultancy firm: “The monthly drop in aggregate EMAE is mainly explained by agriculture: after the record wheat harvest (which affects significantly more in December than in January), agricultural production fell 8% per month without seasonality. The seasonally adjusted EMAE series without agriculture remained stable compared to Dec-25

(0%)”.

For its part, the General Activity Index (IGA) of the consulting firm Orlando Ferreres & Asociados showed a contraction of 1% year-on-year in January, although in seasonally adjusted terms it registered an increase of 0.4% compared to the previous month.

The consultants said: “The activity continues to show two realities, with agriculture, the energy sector and financial intermediation showing a lot of dynamism, and the more labor-intensive sectors, such as industry, commerce and construction, with a much weaker performance. We understand that this dual dynamic will continue in the coming months, with a possible reactivation contingent on the recovery of domestic consumption, hand in hand with better household incomes and the motorization of

credit.”

In parallel, LCG economists argued that, despite recent growth, the pace of expansion could moderate in the short term. “Even with the striking growth in December, which leaves a higher statistical drag (2 pp), we don't expect high growth this year. We continue to project an increase in activity below the 3% annual average based on the traction that a few sectors (oil, mining, agriculture and financial intermediation) may exert

.”

In addition, they added: “For the rest, we did not find drivers that push growth. For the most part, they will continue to be tied to i) weak domestic demand with stagnant wages and the creation of low-quality employment (which is unlikely to be reversed in the short term with the approval of the labor reform), ii) a once again negative fiscal impulse to achieve a stricter fiscal goal this year, and iii) commercial opening in a lower exchange