What explains the jump to USD 37,000 million and what may happen with debt payments and tourism

Nuevo

Agregar La Derecha Diario en

Compartir:

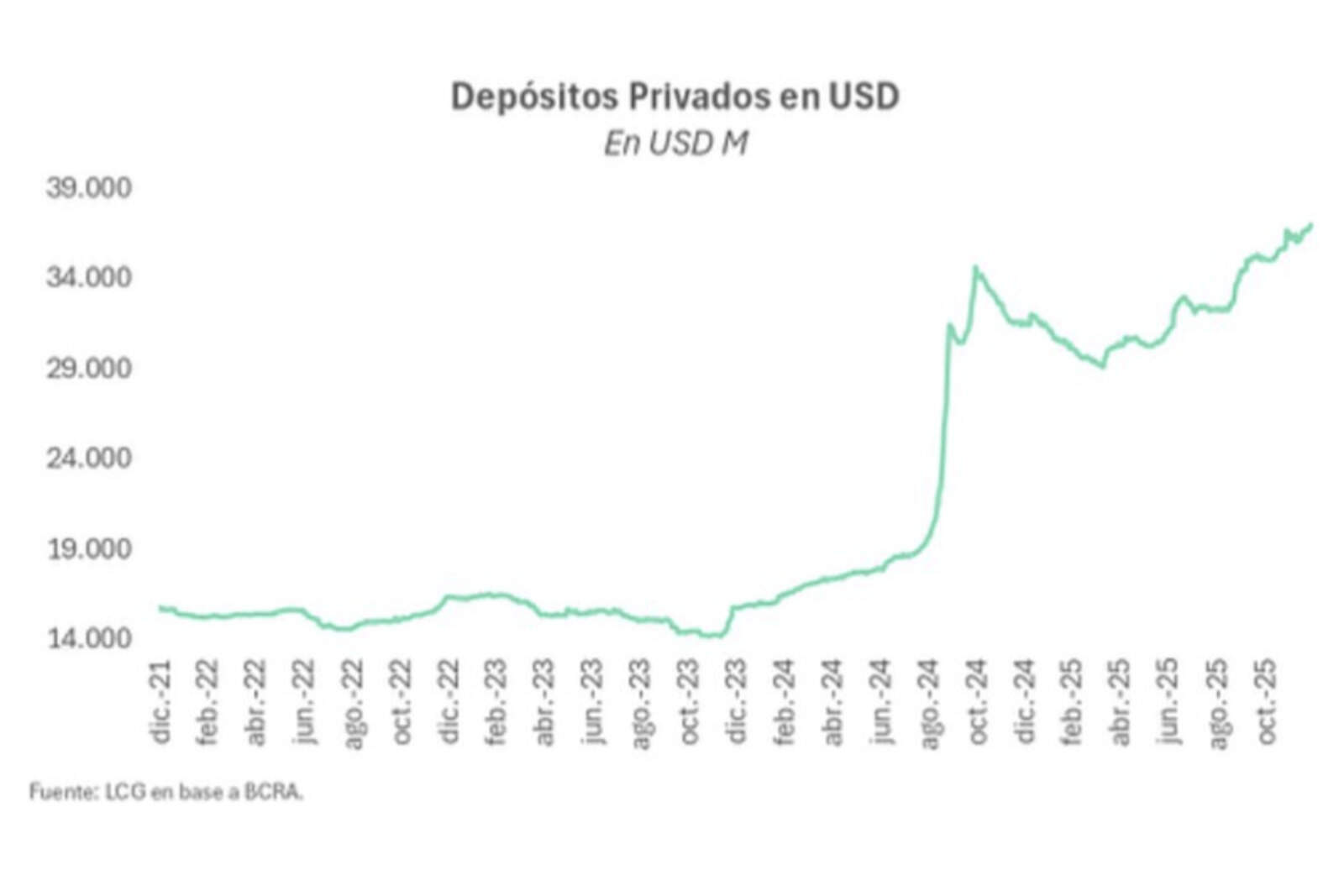

Private sector dollar deposits closed December with a new increase and reached USD 37.006 billion, the highest level since the end of convertibility. The stock grew by USD 1.231 billion in the month.This implies an increase of 3.4%, and it consolidates the recovery from the lows at the end of 2023, when the total was around USD 14 billion.

Depósitos privados en dólares

What explains the jump: stability, confidence, and tax amnesty

The rebound is associated with greater exchange rate stability and an improvement in confidence in the banking system.This led many savers to keep dollars within the institutions instead of withdrawing them in cash.

The official series records these placements as "USD deposits – private sector".This includes savings accounts, checking accounts, and time deposits in foreign currency.

Guillermo Barbero, a partner at First Capital Group, linked the dynamics to several factors: "The increase is linked to the provisions of the tax amnesty, the emergence of new investment alternatives, and a greater degree of certainty regarding the economic framework".

In addition, the growth of dollar loans provided an additional incentive. In the last two years, credit in foreign currency has expanded at a pace close to USD 7 billion per year. Then, with greater demand for financing, banks tend to capture dollars in order to channel them into credit.

Barbero pointed out a change in signals in the market: some institutions began to pay interest on dollar savings accounts, paying interest on those balances. In that context, he warned that keeping dollars outside the system has a cost.

Guardar los dólares “en el colchón” implica una pérdida de valor, ya que la moneda estadounidense también se deprecia por la inflación en Estados Unidos.

Dollar maturities and the seasonal summer effect

In the short term, another relevant factor appears: the schedule of sovereign debt maturities in foreign currency. On January 9, the Government must make payments of more than USD 4.2 billion corresponding to different securities under local and foreign law.

Since an important part of those bonds is in the hands of resident investors, thosedollars could be credited and remain, at least temporarily, within the local banking system.

On that point, economist Amilcar Collante estimated: "Due to the debt payment of the Bonares, dollar deposits will probably increase by around USD 1 billion, and then decrease again, as happened with other previous payments."

El BCRA consiguió un Repo de USD 3.000 millones y garantiza el pago del próximo vencimiento de deuda

He added a seasonal element: "It is to be expected that outbound tourism will have a seasonal impact, since part of those dollars will be used to pay expenses abroad". He also mentioned that the Fiscal Innocence Law could have an influence, although he considered that its effect would be smaller than that of the tax amnesty.

In the same vein, LCG maintained that, going forward, the baseline scenario combines lower macro uncertainty and lower devaluation expectations. Then it said: "The increase in peso deposits is expected to continue and the growth of dollar deposits is expected to moderate", with momentum conditioned by the evolution of exchange rate tensions.

Peso deposits: rebound due to year-end bonuses and stronger demand deposits

Los depósitos en pesos también aumentaron

Peso deposits also rebounded in December: they grew by 5.6%, reversing the decline of the previous two months.This growth was influenced by the payment of year-end bonuses and seasonal year-end factors. The greatest boost came from demand deposits, which increased by 13.3% in real monthly terms.

Within that segment, savings accounts rose by 14.1% in real terms and accounted for 3.7 percentage points of the overall improvement. Meanwhile, checking accounts grew by 12% in real terms and contributed 2.2 points. In contrast, time deposits fell by 2.7% in real monthly terms, the only component that declined in the period.