The stock market posts its sixth consecutive gain, and bonds maintain stability, with country risk at 648 basis points

Compartir:

Argentine stocks and bonds are trading with an upward dynamic this Tuesday, in a year-end that appears promising for prices, although still conditioned by the external environment.

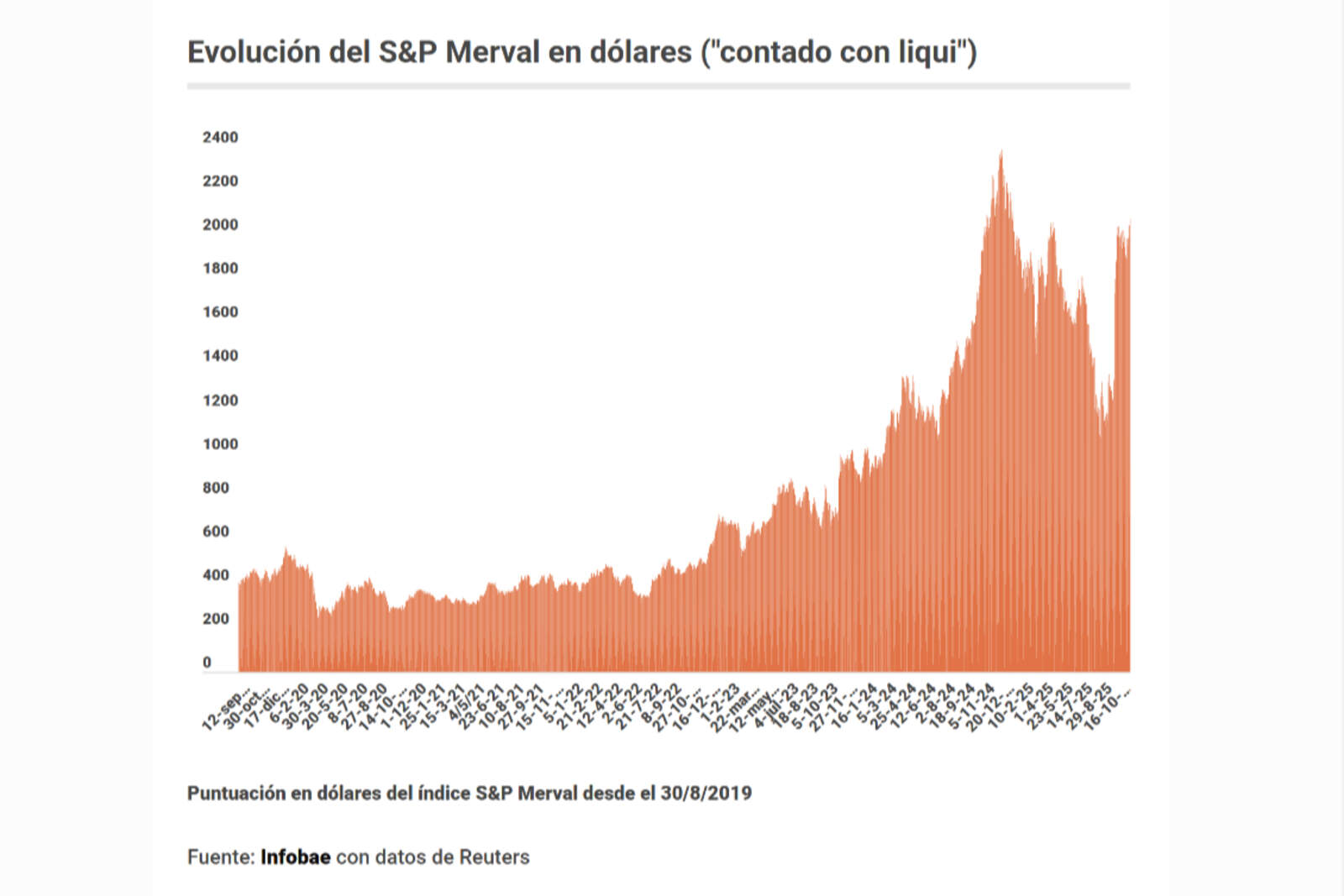

At 11:30, the S&P Merval was up 0.6%, reaching 3,080,000 points, thus chaining its sixth consecutive session in positive territory. In "contado con liquidación" dollars, the panel already exceeds USD 2,000 and is just 4% below the 2023 close.

La Bolsa opera en suba por sexto día

In New York, Argentine ADRs show mixed performance:

Pampa Energía falls 0.5%

Grupo Galicia rises 0.6%

YPF advances 0.6%

Bonds, country risk, and market outlook

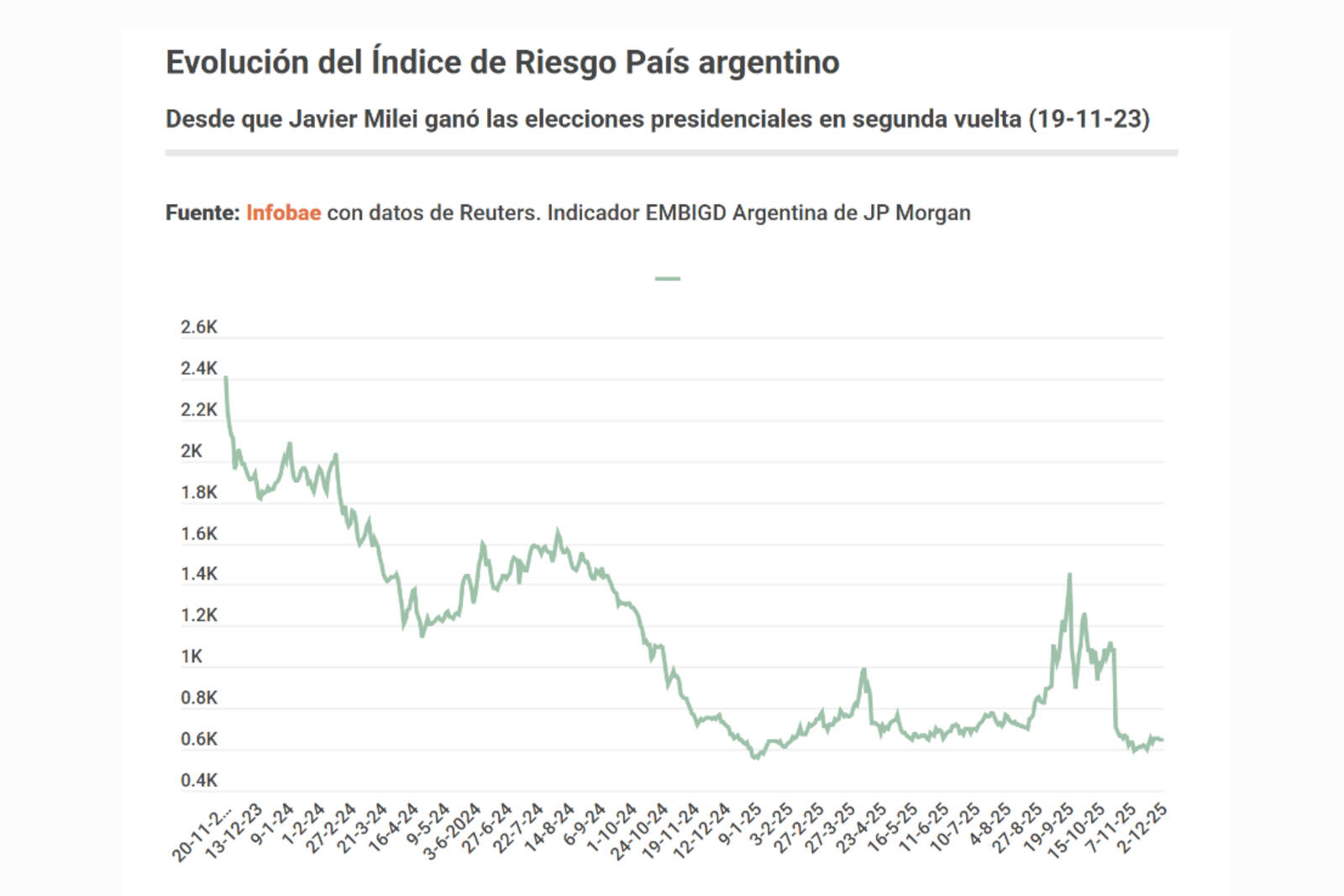

Dollar-denominated bonds —Globales and Bonares— register a marginal improvement of 0.1%, while the country risk index calculated by JP Morgan rises only 1 point, to 648 basis points.

Evolución del Riesgo País

According to analysts at MegaQM, "the recovery of Hard Dollar assets has stalled and the market is still waiting for signals confirming the ability to accumulate reserves". They add: "In any case, we continue to see too wide a gap in the short end between the New York Law curve and the Argentine Law. We expect official moves during December to raise cash and pay January maturities."

Tax revenue: real decline in November

In the real economy, November's tax revenue rose 19.7% year-on-year, which implies a real decrease of 8.9% when considering monthly inflation of around 12.5%.

For Max Capital,"the decline is mainly explained by the high comparison base of the personal assets tax". They state that this is because November 2022 revenues included the special regime, the end of PAIS tax collection, and revenues from the first stage of the tax amnesty, which had boosted last year's figures.

Export duties, measured in real terms, plummeted 69% year-on-year, partly due to early settlements in the first half of 2023 —a result of the temporary reduction in export taxes— and the USD 7 billion advanced under the zero-tariff scheme implemented in September.

Among taxes linked to domestic activity, mixed data are observed in real terms:

VAT: –2.7% year-on-year

Social security: –1.1%

Income tax: –2.9%

Debits and credits: –5.4%

Import tariffs: +21.4%

"VAT, which acts as a leading indicator of activity, recorded a slight contraction, suggesting that economic activity has slowed down," concluded Max Capital.

Foreign trade

A report by the firm Jidoka indicated that exports totaled USD 55.367 billion, an increase of 6.2%, while imports climbed to USD 50.296 billion, a 32.1% year-on-year increase.

"This asymmetry in growth has caused the trade surplus to shrink to USD 5.071 billion, a figure significantly lower than the USD 14.075 billion recorded between January and August 2022. This represents a 64% drop in the positive balance," Jidoka stated.

MegaQM also highlighted that "next week the Fed meets and the market expects a new rate cut. This is despite inflation data that was somewhat higher than expected and employment information —delayed by the shutdown— that turned out better than expected. Soybeans maintain their upward trend and oil has recovered some of what was lost in previous weeks."

Evolución del S&P Merval

Meanwhile, a report by IEB explained that "in recent days, the more moderate voices within the Federal Reserve have gained prominence. As a result, the probability of a rate cut in December rose above 85% at the beginning of this week."

In addition, the U.S. Treasury Secretary, Scott Bessent, announced that "the second round of interviews to select the next Fed chair would be completed on Tuesday and that Donald Trump would announce his decision before Christmas."

That same day, Bloomberg stated that Kevin Hassett is emerging as the main candidate to chair the Fed starting next May.