Searching for data from the BCU to update material for my classes on persistent inflation in Uruguay, I found a news item on its homepage from its monetary policy committee: "April 8, 2025: The BCU increases the interest rate to 9.25% to drive inflation to the target of 4.5%."

In a previous post, I mentioned that the then-future Minister of Economy, Gabriel Oddone, proposed de-indexing wages to prevent the increase in inflation. The article was "De-indexation... Correct Measure for Wrong Reasons."

I will explain why inflation will not remain within the target range (post-lag) and how the background of a government with ideas—which I consider wrong—about how the economy works will also produce the usual low growth with high unemployment.

You might also be interested in: Casmu is saved

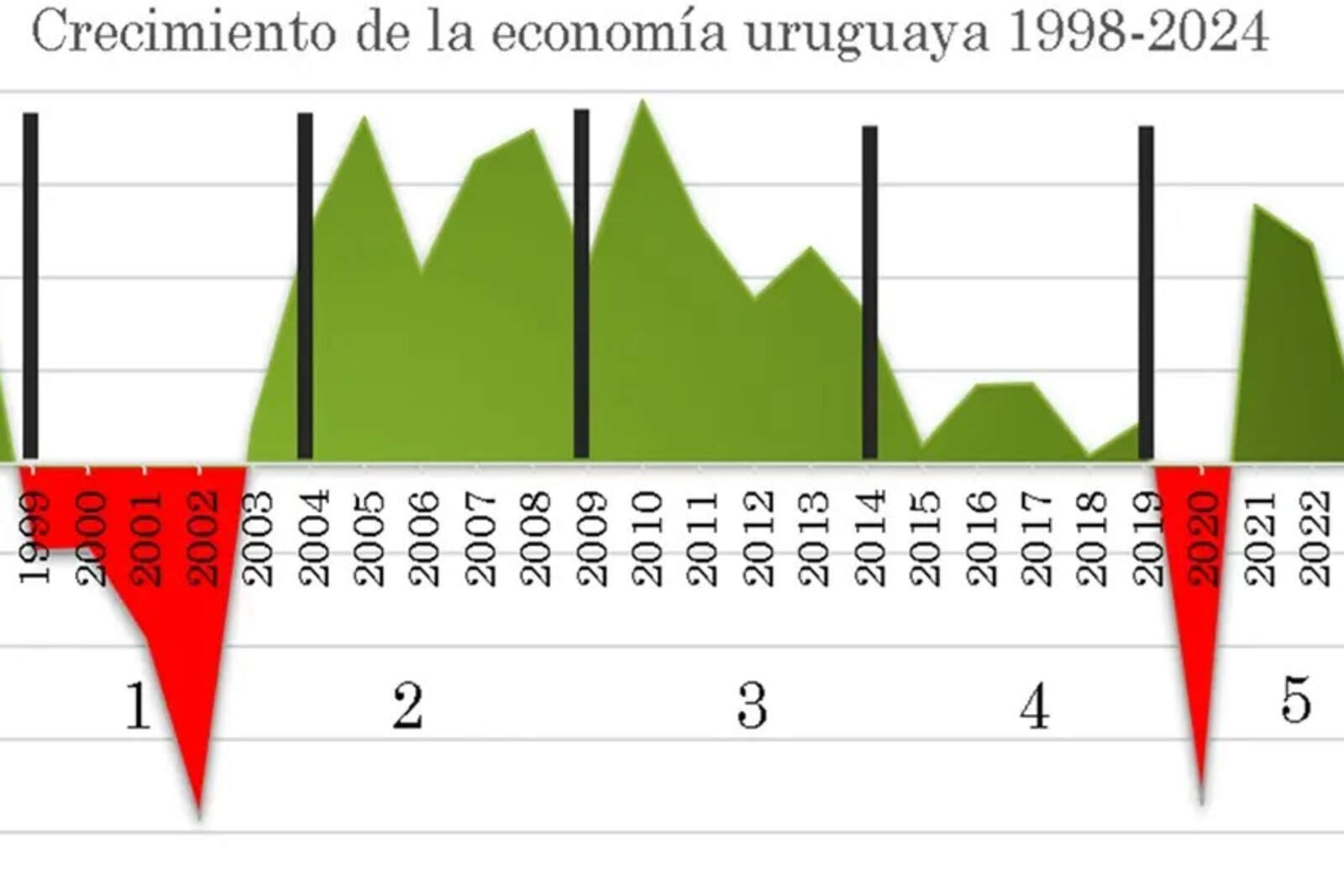

Persistent inflation in Uruguay, the last 25 years

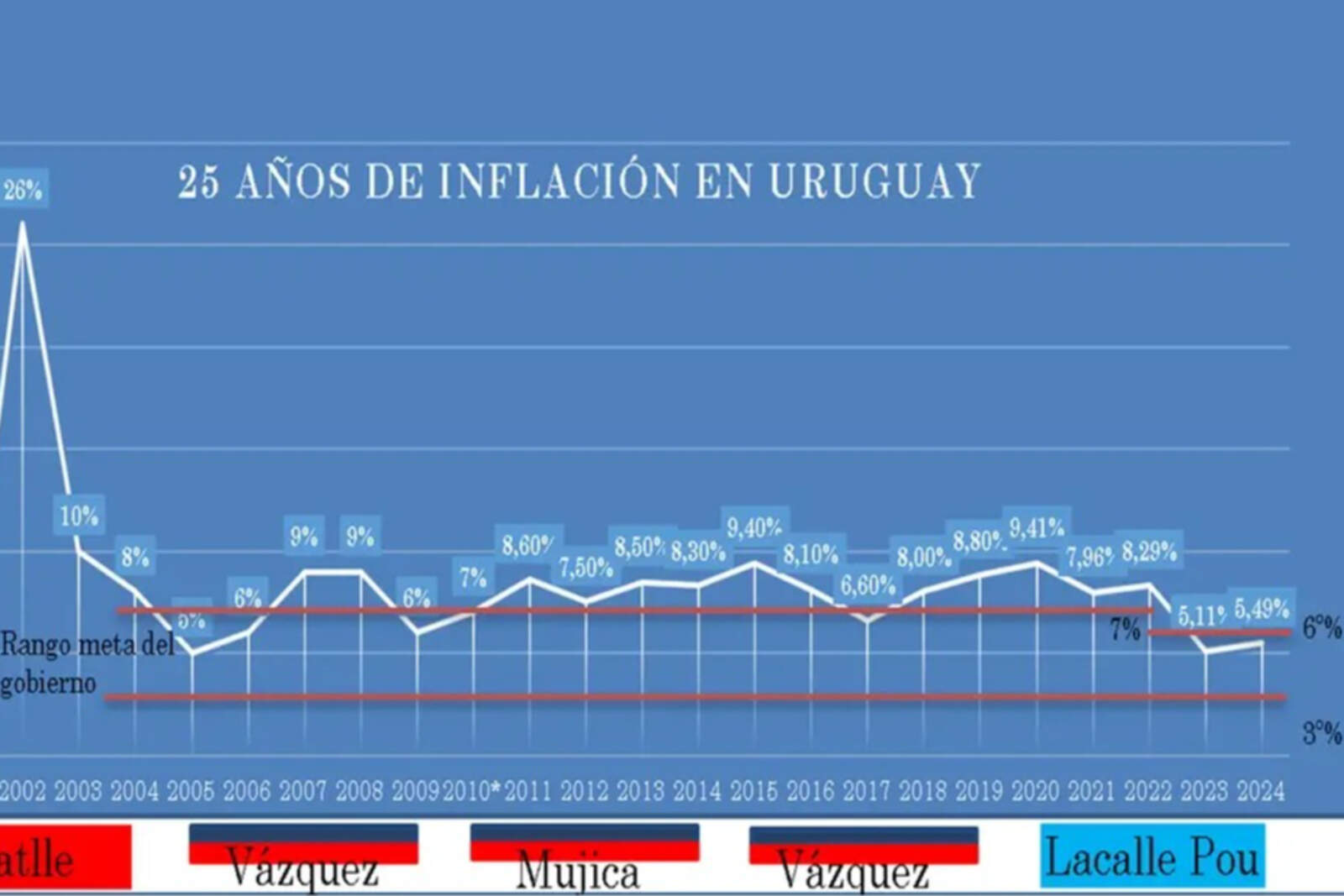

The following table shows inflation in the last five governments, almost always outside the target range since it was implemented, in the 15 years of the same government to the current one, the Vázquez-Mujica-Vázquez period.

About Mujica's role in this period

The largest increase in the CPI was recorded during the 2002 crisis, with 26%. Since 2004, after establishing an annual target range between 3% and 7% (3-6% since September 2022), inflation has rarely been within the bands, although close to the maximum limit.

In times of crisis, as often happens in our case, governments apply Keynesian measures, among others, increase the amount of money as a way to overcome it and encourage recovery. I will also explain this fallacy.

Crisis and insecurity also demand another model

Sole cause of inflation

Inflation is not multi-causal nor a "complex" issue. The cause is the central bank's issuance of money to lend to the government as a means to finance the fiscal deficit. This is not free; we all pay for it with more poverty.

The fiscal deficit occurs every time the government spends more than it collects in taxes.